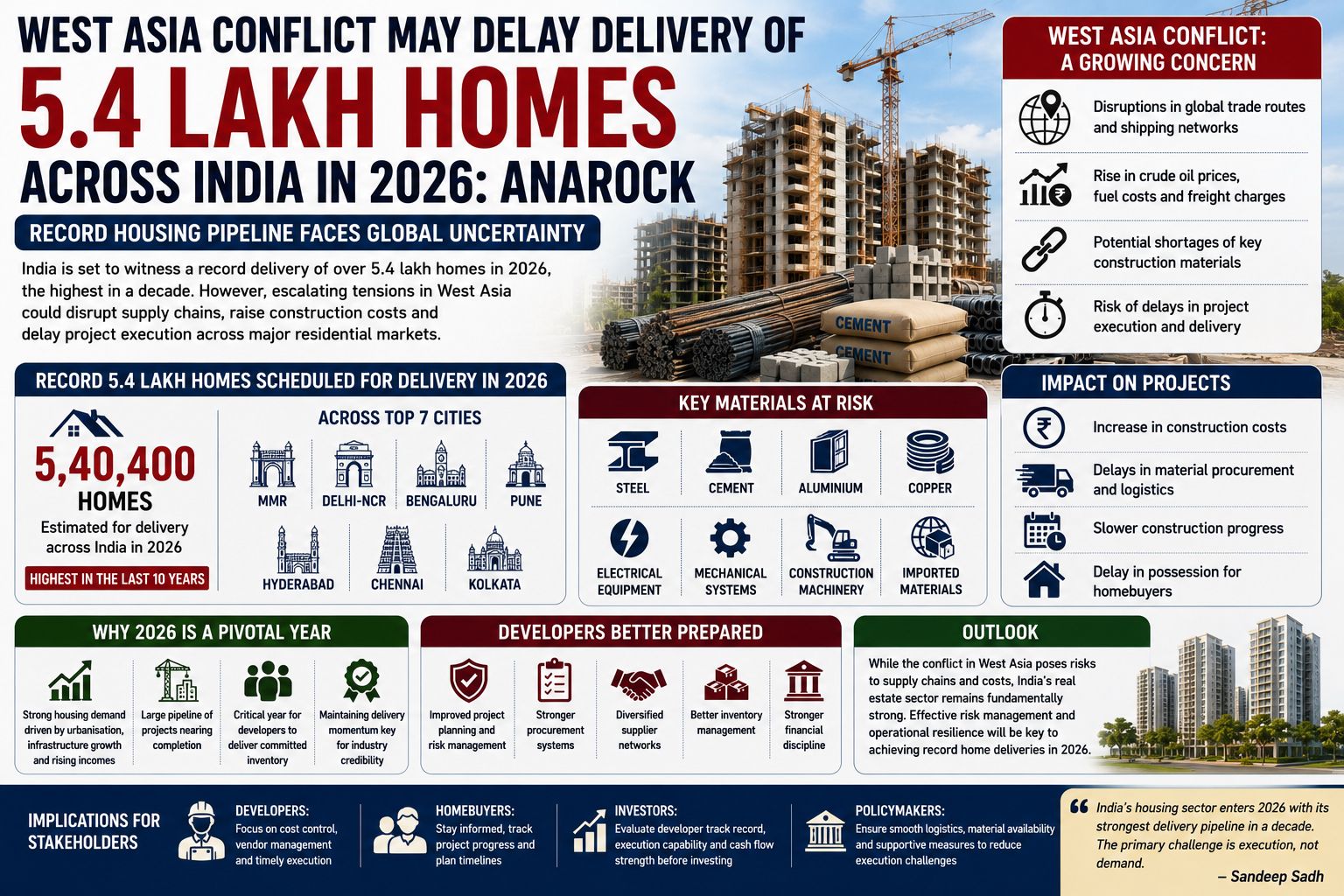

West Asia Conflict Could Delay Delivery of 5.4 Lakh Homes Across India in 2026: Anarock

India Faces Record Housing Delivery Year Amid Global Uncertainty

India's residential real estate sector is preparing for a landmark year, with approximately 5.4 lakh homes scheduled for delivery across the country's top seven cities in 2026. According to housing market estimates, this represents the highest annual delivery volume recorded in the past decade.

The strong pipeline reflects the recovery and expansion witnessed by the housing sector over the last few years, with developers accelerating construction and execution to meet growing demand from end-users.

However, the industry's execution outlook is now facing a fresh challenge. The ongoing conflict in West Asia has created concerns regarding supply-chain disruptions, material costs, logistics availability, and overall project timelines.

Why West Asia Matters to Indian Real Estate

While the conflict is geographically distant from India, its economic impact could directly affect the construction sector.

The Middle East plays a critical role in global trade routes, energy markets, shipping networks, and commodity pricing. Any prolonged disruption can increase transportation costs and affect the movement of raw materials used in construction.

Real estate projects depend heavily on inputs such as:

- Steel

- Cement

- Aluminium

- Copper

- Electrical equipment

- Mechanical systems

- Construction machinery

- Imported building materials

Any increase in logistics costs or supply shortages can affect project budgets and construction schedules.

Developers are therefore closely monitoring global developments and their potential impact on project execution.

Record 5.4 Lakh Homes Scheduled for Delivery

The estimated 5,40,400 housing units planned for completion in 2026 represent a significant milestone for India's residential market.

The large delivery pipeline is spread across the country's major residential centres, including:

- Mumbai Metropolitan Region (MMR)

- Delhi-NCR

- Bengaluru

- Pune

- Hyderabad

- Chennai

- Kolkata

Many of these projects were launched during the post-pandemic recovery phase and are now approaching completion.

Successful delivery of this inventory is critical not only for developers but also for thousands of homebuyers awaiting possession.

Construction Costs Could Rise Again

One of the biggest concerns arising from the conflict is the possibility of rising construction costs.

Historically, geopolitical tensions in energy-producing regions have led to increases in:

- Crude oil prices

- Fuel costs

- Freight charges

- Commodity prices

Since construction is highly dependent on transportation and energy, higher input costs can directly impact project economics.

Developers may face pressure on margins if material costs rise unexpectedly after projects have already been sold.

Projects under construction could therefore encounter financial and execution challenges if volatility continues for an extended period.

Supply Chains Remain Vulnerable

The real estate industry has only recently recovered from earlier supply-chain disruptions caused by the pandemic and global logistics bottlenecks.

Many developers have spent the past few years rebuilding procurement networks and improving construction schedules.

A prolonged conflict could once again create uncertainty around:

- Import timelines

- Equipment availability

- Shipping schedules

- Construction materials

- Infrastructure project supplies

Large projects that rely on specialised imported systems may face greater exposure to delays.

Developers with strong procurement planning and diversified supplier networks are likely to be better positioned to manage disruptions.

Mumbai Could Feel the Impact

Mumbai remains one of India's largest housing markets and has a substantial volume of projects under construction.

The city's redevelopment pipeline, luxury housing launches, infrastructure-linked projects, and large township developments require significant quantities of construction materials and engineering systems.

Any disruption to supply chains could affect project execution schedules across:

- Redevelopment projects

- Slum rehabilitation schemes

- Premium residential developments

- Commercial projects

- Integrated townships

While developers generally maintain inventory buffers, prolonged volatility could still impact delivery timelines.

Homebuyers Awaiting Possession May Be Affected

The biggest concern for buyers is the possibility of delayed possession.

Over the last few years, developers have worked aggressively to improve delivery records and comply with RERA commitments.

A rise in material shortages, transportation delays, or labour disruptions could slow construction progress at some projects.

While there is currently no indication of widespread delays, industry participants are closely monitoring the situation.

Buyers awaiting possession should continue tracking project progress and official communications from developers.

Developers Better Prepared Than Before

Despite the risks, many industry experts believe the sector is now better prepared to manage external shocks than it was during previous disruptions.

Developers have:

- Improved project planning

- Strengthened procurement systems

- Increased inventory management

- Diversified supplier networks

- Enhanced financial discipline

The industry's experience during the pandemic has encouraged companies to build greater resilience into project execution strategies.

This may help limit the severity of any future disruptions.

Strong Housing Demand Continues

Importantly, the conflict has not altered the underlying demand fundamentals of India's housing market.

Residential demand remains supported by:

- Urbanisation

- Infrastructure development

- End-user buying activity

- Stable employment trends

- Growing middle-class incomes

The current concern is primarily related to execution and delivery rather than demand.

If supply-chain pressures remain manageable, developers could still achieve a substantial portion of the planned deliveries during the year.

Implications for Real Estate Investors

For investors, the situation highlights the importance of evaluating project execution capabilities rather than focusing solely on location and pricing.

Developers with strong balance sheets, established procurement systems, and proven delivery records may be better positioned to navigate global uncertainties.

Projects nearing completion may also face lower execution risk compared to newly launched developments.

As global events continue to influence construction economics, execution quality is becoming an increasingly important factor in investment decisions.

The Road Ahead

The delivery of over 5.4 lakh homes in 2026 represents a major opportunity for India's residential sector. However, the evolving situation in West Asia introduces an element of uncertainty that developers cannot ignore.

The industry's ability to manage supply-chain risks, control costs, and maintain construction schedules will determine whether this record delivery pipeline translates into successful handovers.

For now, the housing market remains fundamentally strong, but the coming months will be crucial in assessing how global geopolitical developments affect project execution across India.

Expert View

"India's housing sector enters 2026 with its strongest delivery pipeline in a decade. The primary challenge is no longer demand but execution. Developers who can effectively manage procurement, logistics, and cost pressures will be best positioned to deliver homes on schedule despite global uncertainties." — Sandeep Sadh